Conditional Average Treatment Effects (CATE) with DoWhy and EconML

This is an experimental feature where we use EconML methods from DoWhy. Using EconML allows CATE estimation using different methods.

All four steps of causal inference in DoWhy remain the same: model, identify, estimate, and refute. The key difference is that we now call econml methods in the estimation step. There is also a simpler example using linear regression to understand the intuition behind CATE estimators.

All datasets are generated using linear structural equations.

[1]:

%load_ext autoreload

%autoreload 2

[2]:

import numpy as np

import pandas as pd

import logging

import dowhy

from dowhy import CausalModel

import dowhy.datasets

import econml

import warnings

warnings.filterwarnings('ignore')

BETA = 10

[3]:

data = dowhy.datasets.linear_dataset(BETA, num_common_causes=4, num_samples=10000,

num_instruments=2, num_effect_modifiers=2,

num_treatments=1,

treatment_is_binary=False,

num_discrete_common_causes=2,

num_discrete_effect_modifiers=0,

one_hot_encode=False)

df=data['df']

print(df.head())

print("True causal estimate is", data["ate"])

X0 X1 Z0 Z1 W0 W1 W2 W3 v0 \

0 -0.533201 -1.022194 0.0 0.179820 -0.126268 -0.665279 0 2 0.377309

1 1.922557 -0.762009 0.0 0.899564 -0.229440 -1.197794 1 1 9.944403

2 1.171414 1.479419 1.0 0.513904 0.987447 0.439091 0 2 24.655594

3 0.484425 -1.845972 0.0 0.387353 1.517763 -0.685227 0 3 13.782830

4 1.122992 0.385469 0.0 0.313835 0.115356 2.225336 1 1 17.397334

y

0 1.888306

1 84.051100

2 399.830888

3 65.517166

4 220.655496

True causal estimate is 9.049694403977

[4]:

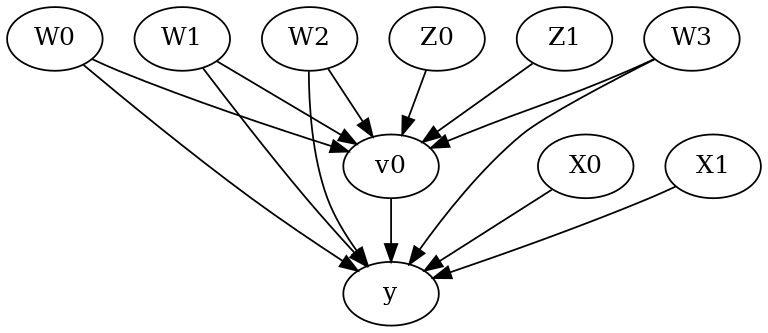

model = CausalModel(data=data["df"],

treatment=data["treatment_name"], outcome=data["outcome_name"],

graph=data["gml_graph"])

[5]:

model.view_model()

from IPython.display import Image, display

display(Image(filename="causal_model.png"))

[6]:

identified_estimand= model.identify_effect(proceed_when_unidentifiable=True)

print(identified_estimand)

Estimand type: nonparametric-ate

### Estimand : 1

Estimand name: backdoor

Estimand expression:

d

─────(E[y|W2,W0,W1,W3])

d[v₀]

Estimand assumption 1, Unconfoundedness: If U→{v0} and U→y then P(y|v0,W2,W0,W1,W3,U) = P(y|v0,W2,W0,W1,W3)

### Estimand : 2

Estimand name: iv

Estimand expression:

⎡ -1⎤

⎢ d ⎛ d ⎞ ⎥

E⎢─────────(y)⋅⎜─────────([v₀])⎟ ⎥

⎣d[Z₀ Z₁] ⎝d[Z₀ Z₁] ⎠ ⎦

Estimand assumption 1, As-if-random: If U→→y then ¬(U →→{Z0,Z1})

Estimand assumption 2, Exclusion: If we remove {Z0,Z1}→{v0}, then ¬({Z0,Z1}→y)

### Estimand : 3

Estimand name: frontdoor

No such variable(s) found!

Linear Model

First, let us build some intuition using a linear model for estimating CATE. The effect modifiers (that lead to a heterogeneous treatment effect) can be modeled as interaction terms with the treatment. Thus, their value modulates the effect of treatment.

Below the estimated effect of changing treatment from 0 to 1.

[7]:

linear_estimate = model.estimate_effect(identified_estimand,

method_name="backdoor.linear_regression",

control_value=0,

treatment_value=1)

print(linear_estimate)

*** Causal Estimate ***

## Identified estimand

Estimand type: nonparametric-ate

### Estimand : 1

Estimand name: backdoor

Estimand expression:

d

─────(E[y|W2,W0,W1,W3])

d[v₀]

Estimand assumption 1, Unconfoundedness: If U→{v0} and U→y then P(y|v0,W2,W0,W1,W3,U) = P(y|v0,W2,W0,W1,W3)

## Realized estimand

b: y~v0+W2+W0+W1+W3+v0*X0+v0*X1

Target units: ate

## Estimate

Mean value: 9.049415183121157

### Conditional Estimates

__categorical__X0 __categorical__X1

(-3.5749999999999997, -0.687] (-4.484, -1.15] 3.288129

(-1.15, -0.562] 6.267303

(-0.562, -0.0573] 8.040084

(-0.0573, 0.538] 9.904973

(0.538, 3.207] 12.728653

(-0.687, -0.0947] (-4.484, -1.15] 3.897843

(-1.15, -0.562] 6.885845

(-0.562, -0.0573] 8.702318

(-0.0573, 0.538] 10.441822

(0.538, 3.207] 13.349133

(-0.0947, 0.407] (-4.484, -1.15] 4.452250

(-1.15, -0.562] 7.266740

(-0.562, -0.0573] 9.058710

(-0.0573, 0.538] 10.834069

(0.538, 3.207] 13.682690

(0.407, 0.987] (-4.484, -1.15] 4.755422

(-1.15, -0.562] 7.603704

(-0.562, -0.0573] 9.435272

(-0.0573, 0.538] 11.217643

(0.538, 3.207] 14.214437

(0.987, 4.197] (-4.484, -1.15] 5.298979

(-1.15, -0.562] 8.278518

(-0.562, -0.0573] 10.018361

(-0.0573, 0.538] 11.803522

(0.538, 3.207] 14.808277

dtype: float64

EconML methods

We now move to the more advanced methods from the EconML package for estimating CATE.

First, let us look at the double machine learning estimator. Method_name corresponds to the fully qualified name of the class that we want to use. For double ML, it is “econml.dml.DML”.

Target units defines the units over which the causal estimate is to be computed. This can be a lambda function filter on the original dataframe, a new Pandas dataframe, or a string corresponding to the three main kinds of target units (“ate”, “att” and “atc”). Below we show an example of a lambda function.

Method_params are passed directly to EconML. For details on allowed parameters, refer to the EconML documentation.

[8]:

from sklearn.preprocessing import PolynomialFeatures

from sklearn.linear_model import LassoCV

from sklearn.ensemble import GradientBoostingRegressor

dml_estimate = model.estimate_effect(identified_estimand, method_name="backdoor.econml.dml.DML",

control_value = 0,

treatment_value = 1,

target_units = lambda df: df["X0"]>1, # condition used for CATE

confidence_intervals=False,

method_params={"init_params":{'model_y':GradientBoostingRegressor(),

'model_t': GradientBoostingRegressor(),

"model_final":LassoCV(fit_intercept=False),

'featurizer':PolynomialFeatures(degree=1, include_bias=False)},

"fit_params":{}})

print(dml_estimate)

2022-09-14 18:44:20.050299: W tensorflow/stream_executor/platform/default/dso_loader.cc:64] Could not load dynamic library 'libcudart.so.11.0'; dlerror: libcudart.so.11.0: cannot open shared object file: No such file or directory

2022-09-14 18:44:20.050337: I tensorflow/stream_executor/cuda/cudart_stub.cc:29] Ignore above cudart dlerror if you do not have a GPU set up on your machine.

*** Causal Estimate ***

## Identified estimand

Estimand type: nonparametric-ate

### Estimand : 1

Estimand name: backdoor

Estimand expression:

d

─────(E[y|W2,W0,W1,W3])

d[v₀]

Estimand assumption 1, Unconfoundedness: If U→{v0} and U→y then P(y|v0,W2,W0,W1,W3,U) = P(y|v0,W2,W0,W1,W3)

## Realized estimand

b: y~v0+W2+W0+W1+W3 | X0,X1

Target units: Data subset defined by a function

## Estimate

Mean value: 10.073101008999998

Effect estimates: [ 8.75174232 15.87229533 12.10883134 ... 7.61828507 2.48628422

9.32302822]

[9]:

print("True causal estimate is", data["ate"])

True causal estimate is 9.049694403977

[10]:

dml_estimate = model.estimate_effect(identified_estimand, method_name="backdoor.econml.dml.DML",

control_value = 0,

treatment_value = 1,

target_units = 1, # condition used for CATE

confidence_intervals=False,

method_params={"init_params":{'model_y':GradientBoostingRegressor(),

'model_t': GradientBoostingRegressor(),

"model_final":LassoCV(fit_intercept=False),

'featurizer':PolynomialFeatures(degree=1, include_bias=True)},

"fit_params":{}})

print(dml_estimate)

*** Causal Estimate ***

## Identified estimand

Estimand type: nonparametric-ate

### Estimand : 1

Estimand name: backdoor

Estimand expression:

d

─────(E[y|W2,W0,W1,W3])

d[v₀]

Estimand assumption 1, Unconfoundedness: If U→{v0} and U→y then P(y|v0,W2,W0,W1,W3,U) = P(y|v0,W2,W0,W1,W3)

## Realized estimand

b: y~v0+W2+W0+W1+W3 | X0,X1

Target units:

## Estimate

Mean value: 9.0105851188843

Effect estimates: [ 6.15557119 8.64699923 15.73603354 ... 15.87179788 8.05935455

8.75923011]

CATE Object and Confidence Intervals

EconML provides its own methods to compute confidence intervals. Using BootstrapInference in the example below.

[11]:

from sklearn.preprocessing import PolynomialFeatures

from sklearn.linear_model import LassoCV

from sklearn.ensemble import GradientBoostingRegressor

from econml.inference import BootstrapInference

dml_estimate = model.estimate_effect(identified_estimand,

method_name="backdoor.econml.dml.DML",

target_units = "ate",

confidence_intervals=True,

method_params={"init_params":{'model_y':GradientBoostingRegressor(),

'model_t': GradientBoostingRegressor(),

"model_final": LassoCV(fit_intercept=False),

'featurizer':PolynomialFeatures(degree=1, include_bias=True)},

"fit_params":{

'inference': BootstrapInference(n_bootstrap_samples=100, n_jobs=-1),

}

})

print(dml_estimate)

*** Causal Estimate ***

## Identified estimand

Estimand type: nonparametric-ate

### Estimand : 1

Estimand name: backdoor

Estimand expression:

d

─────(E[y|W2,W0,W1,W3])

d[v₀]

Estimand assumption 1, Unconfoundedness: If U→{v0} and U→y then P(y|v0,W2,W0,W1,W3,U) = P(y|v0,W2,W0,W1,W3)

## Realized estimand

b: y~v0+W2+W0+W1+W3 | X0,X1

Target units: ate

## Estimate

Mean value: 8.97103120997889

Effect estimates: [ 6.11637397 8.57762811 15.70466462 ... 15.84544308 8.00633323

8.73332712]

95.0% confidence interval: (array([ 6.04294108, 8.42758643, 15.77291365, ..., 15.92144005,

7.93937896, 8.75143052]), array([ 6.18996505, 8.66689443, 16.17018427, ..., 16.33172413,

8.06900788, 8.91158551]))

Can provide a new inputs as target units and estimate CATE on them.

[12]:

test_cols= data['effect_modifier_names'] # only need effect modifiers' values

test_arr = [np.random.uniform(0,1, 10) for _ in range(len(test_cols))] # all variables are sampled uniformly, sample of 10

test_df = pd.DataFrame(np.array(test_arr).transpose(), columns=test_cols)

dml_estimate = model.estimate_effect(identified_estimand,

method_name="backdoor.econml.dml.DML",

target_units = test_df,

confidence_intervals=False,

method_params={"init_params":{'model_y':GradientBoostingRegressor(),

'model_t': GradientBoostingRegressor(),

"model_final":LassoCV(),

'featurizer':PolynomialFeatures(degree=1, include_bias=True)},

"fit_params":{}

})

print(dml_estimate.cate_estimates)

[11.04119185 13.14994662 10.35837984 12.47894912 11.36113085 13.39935511

13.90418027 10.28889381 12.38958317 12.97335591]

Can also retrieve the raw EconML estimator object for any further operations

[13]:

print(dml_estimate._estimator_object)

<econml.dml.dml.DML object at 0x7f0cf55373a0>

Works with any EconML method

In addition to double machine learning, below we example analyses using orthogonal forests, DRLearner (bug to fix), and neural network-based instrumental variables.

Binary treatment, Binary outcome

[14]:

data_binary = dowhy.datasets.linear_dataset(BETA, num_common_causes=4, num_samples=10000,

num_instruments=2, num_effect_modifiers=2,

treatment_is_binary=True, outcome_is_binary=True)

# convert boolean values to {0,1} numeric

data_binary['df'].v0 = data_binary['df'].v0.astype(int)

data_binary['df'].y = data_binary['df'].y.astype(int)

print(data_binary['df'])

model_binary = CausalModel(data=data_binary["df"],

treatment=data_binary["treatment_name"], outcome=data_binary["outcome_name"],

graph=data_binary["gml_graph"])

identified_estimand_binary = model_binary.identify_effect(proceed_when_unidentifiable=True)

X0 X1 Z0 Z1 W0 W1 W2 \

0 -0.977022 1.067383 1.0 0.696816 0.877629 -0.704097 -2.705619

1 0.119435 1.646813 1.0 0.932599 1.045068 -1.503361 -0.811373

2 2.368885 2.055748 1.0 0.551497 0.832655 -0.056771 -2.144246

3 -0.256994 0.945261 1.0 0.614187 -1.904988 -1.624514 -1.838845

4 2.329471 1.215418 1.0 0.647074 2.402067 -0.312094 -1.590205

... ... ... ... ... ... ... ...

9995 1.327564 3.895272 0.0 0.974441 1.724229 -0.534615 0.062941

9996 0.095342 1.142415 1.0 0.890541 1.315665 -0.436278 -0.964123

9997 0.909117 1.771237 1.0 0.402906 1.189027 -0.175096 -0.514647

9998 0.199285 2.383161 1.0 0.166742 -1.331729 -0.409680 -0.525951

9999 2.682434 0.140926 1.0 0.880121 0.744858 -0.319757 -1.370824

W3 v0 y

0 -1.050106 1 1

1 -0.392080 1 1

2 -1.936656 1 1

3 0.332871 1 1

4 -0.294840 1 1

... ... .. ..

9995 -1.546670 1 1

9996 0.571672 1 1

9997 -1.751814 1 1

9998 -0.603038 1 1

9999 -0.995968 1 1

[10000 rows x 10 columns]

Using DRLearner estimator

[15]:

from sklearn.linear_model import LogisticRegressionCV

#todo needs binary y

drlearner_estimate = model_binary.estimate_effect(identified_estimand_binary,

method_name="backdoor.econml.drlearner.LinearDRLearner",

confidence_intervals=False,

method_params={"init_params":{

'model_propensity': LogisticRegressionCV(cv=3, solver='lbfgs', multi_class='auto')

},

"fit_params":{}

})

print(drlearner_estimate)

print("True causal estimate is", data_binary["ate"])

*** Causal Estimate ***

## Identified estimand

Estimand type: nonparametric-ate

### Estimand : 1

Estimand name: backdoor

Estimand expression:

d

─────(E[y|W2,W0,W1,W3])

d[v₀]

Estimand assumption 1, Unconfoundedness: If U→{v0} and U→y then P(y|v0,W2,W0,W1,W3,U) = P(y|v0,W2,W0,W1,W3)

## Realized estimand

b: y~v0+W2+W0+W1+W3 | X0,X1

Target units: ate

## Estimate

Mean value: 0.6073356972078376

Effect estimates: [0.64530812 0.64334411 0.61774472 ... 0.633828 0.66240192 0.55963395]

True causal estimate is 0.4818

Instrumental Variable Method

[16]:

import keras

from econml.deepiv import DeepIVEstimator

dims_zx = len(model.get_instruments())+len(model.get_effect_modifiers())

dims_tx = len(model._treatment)+len(model.get_effect_modifiers())

treatment_model = keras.Sequential([keras.layers.Dense(128, activation='relu', input_shape=(dims_zx,)), # sum of dims of Z and X

keras.layers.Dropout(0.17),

keras.layers.Dense(64, activation='relu'),

keras.layers.Dropout(0.17),

keras.layers.Dense(32, activation='relu'),

keras.layers.Dropout(0.17)])

response_model = keras.Sequential([keras.layers.Dense(128, activation='relu', input_shape=(dims_tx,)), # sum of dims of T and X

keras.layers.Dropout(0.17),

keras.layers.Dense(64, activation='relu'),

keras.layers.Dropout(0.17),

keras.layers.Dense(32, activation='relu'),

keras.layers.Dropout(0.17),

keras.layers.Dense(1)])

deepiv_estimate = model.estimate_effect(identified_estimand,

method_name="iv.econml.deepiv.DeepIV",

target_units = lambda df: df["X0"]>-1,

confidence_intervals=False,

method_params={"init_params":{'n_components': 10, # Number of gaussians in the mixture density networks

'm': lambda z, x: treatment_model(keras.layers.concatenate([z, x])), # Treatment model,

"h": lambda t, x: response_model(keras.layers.concatenate([t, x])), # Response model

'n_samples': 1, # Number of samples used to estimate the response

'first_stage_options': {'epochs':25},

'second_stage_options': {'epochs':25}

},

"fit_params":{}})

print(deepiv_estimate)

2022-09-14 18:47:39.639288: W tensorflow/stream_executor/platform/default/dso_loader.cc:64] Could not load dynamic library 'libcuda.so.1'; dlerror: libcuda.so.1: cannot open shared object file: No such file or directory

2022-09-14 18:47:39.639334: W tensorflow/stream_executor/cuda/cuda_driver.cc:269] failed call to cuInit: UNKNOWN ERROR (303)

2022-09-14 18:47:39.639362: I tensorflow/stream_executor/cuda/cuda_diagnostics.cc:156] kernel driver does not appear to be running on this host (37c5f4ec8b0f): /proc/driver/nvidia/version does not exist

2022-09-14 18:47:39.639675: I tensorflow/core/platform/cpu_feature_guard.cc:193] This TensorFlow binary is optimized with oneAPI Deep Neural Network Library (oneDNN) to use the following CPU instructions in performance-critical operations: AVX2 AVX512F FMA

To enable them in other operations, rebuild TensorFlow with the appropriate compiler flags.

Epoch 1/25

313/313 [==============================] - 1s 2ms/step - loss: 11.9591

Epoch 2/25

313/313 [==============================] - 1s 2ms/step - loss: 4.0460

Epoch 3/25

313/313 [==============================] - 1s 2ms/step - loss: 3.3135

Epoch 4/25

313/313 [==============================] - 1s 2ms/step - loss: 2.7917

Epoch 5/25

313/313 [==============================] - 1s 2ms/step - loss: 2.6947

Epoch 6/25

313/313 [==============================] - 1s 2ms/step - loss: 2.6366

Epoch 7/25

313/313 [==============================] - 1s 2ms/step - loss: 2.6077

Epoch 8/25

313/313 [==============================] - 1s 2ms/step - loss: 2.5855

Epoch 9/25

313/313 [==============================] - 1s 2ms/step - loss: 2.5629

Epoch 10/25

313/313 [==============================] - 1s 2ms/step - loss: 2.5409

Epoch 11/25

313/313 [==============================] - 1s 2ms/step - loss: 2.5363

Epoch 12/25

313/313 [==============================] - 1s 2ms/step - loss: 2.5217

Epoch 13/25

313/313 [==============================] - 1s 2ms/step - loss: 2.5183

Epoch 14/25

313/313 [==============================] - 1s 2ms/step - loss: 2.5099

Epoch 15/25

313/313 [==============================] - 1s 2ms/step - loss: 2.5105

Epoch 16/25

313/313 [==============================] - 1s 2ms/step - loss: 2.5087

Epoch 17/25

313/313 [==============================] - 1s 2ms/step - loss: 2.4881

Epoch 18/25

313/313 [==============================] - 1s 2ms/step - loss: 2.4904

Epoch 19/25

313/313 [==============================] - 1s 2ms/step - loss: 2.4946

Epoch 20/25

313/313 [==============================] - 1s 2ms/step - loss: 2.4887

Epoch 21/25

313/313 [==============================] - 1s 2ms/step - loss: 2.4925

Epoch 22/25

313/313 [==============================] - 1s 2ms/step - loss: 2.4871

Epoch 23/25

313/313 [==============================] - 1s 2ms/step - loss: 2.4811

Epoch 24/25

313/313 [==============================] - 1s 2ms/step - loss: 2.4775

Epoch 25/25

313/313 [==============================] - 1s 2ms/step - loss: 2.4735

Epoch 1/25

313/313 [==============================] - 2s 2ms/step - loss: 21077.2461

Epoch 2/25

313/313 [==============================] - 1s 2ms/step - loss: 10133.7412

Epoch 3/25

313/313 [==============================] - 1s 2ms/step - loss: 8876.9043

Epoch 4/25

313/313 [==============================] - 1s 2ms/step - loss: 8798.7510

Epoch 5/25

313/313 [==============================] - 1s 2ms/step - loss: 8595.7393

Epoch 6/25

313/313 [==============================] - 1s 2ms/step - loss: 8717.2373

Epoch 7/25

313/313 [==============================] - 1s 2ms/step - loss: 8639.3955

Epoch 8/25

313/313 [==============================] - 1s 2ms/step - loss: 8385.5654

Epoch 9/25

313/313 [==============================] - 1s 2ms/step - loss: 8489.7207

Epoch 10/25

313/313 [==============================] - 1s 2ms/step - loss: 8431.2227

Epoch 11/25

313/313 [==============================] - 1s 2ms/step - loss: 8506.2080

Epoch 12/25

313/313 [==============================] - 1s 2ms/step - loss: 8443.2041

Epoch 13/25

313/313 [==============================] - 1s 2ms/step - loss: 8480.6875

Epoch 14/25

313/313 [==============================] - 1s 2ms/step - loss: 8212.8369

Epoch 15/25

313/313 [==============================] - 1s 2ms/step - loss: 8410.5000

Epoch 16/25

313/313 [==============================] - 1s 2ms/step - loss: 8186.9043

Epoch 17/25

313/313 [==============================] - 1s 2ms/step - loss: 8367.1201

Epoch 18/25

313/313 [==============================] - 1s 2ms/step - loss: 8283.7197

Epoch 19/25

313/313 [==============================] - 1s 2ms/step - loss: 8472.3135

Epoch 20/25

313/313 [==============================] - 1s 2ms/step - loss: 8411.8926

Epoch 21/25

313/313 [==============================] - 1s 2ms/step - loss: 8463.8564

Epoch 22/25

313/313 [==============================] - 1s 2ms/step - loss: 8485.9541

Epoch 23/25

313/313 [==============================] - 1s 2ms/step - loss: 8202.4541

Epoch 24/25

313/313 [==============================] - 1s 3ms/step - loss: 8426.0312

Epoch 25/25

313/313 [==============================] - 1s 2ms/step - loss: 8251.6318

WARNING:tensorflow:

The following Variables were used a Lambda layer's call (lambda_7), but

are not present in its tracked objects:

<tf.Variable 'dense_3/kernel:0' shape=(3, 128) dtype=float32>

<tf.Variable 'dense_3/bias:0' shape=(128,) dtype=float32>

<tf.Variable 'dense_4/kernel:0' shape=(128, 64) dtype=float32>

<tf.Variable 'dense_4/bias:0' shape=(64,) dtype=float32>

<tf.Variable 'dense_5/kernel:0' shape=(64, 32) dtype=float32>

<tf.Variable 'dense_5/bias:0' shape=(32,) dtype=float32>

<tf.Variable 'dense_6/kernel:0' shape=(32, 1) dtype=float32>

<tf.Variable 'dense_6/bias:0' shape=(1,) dtype=float32>

It is possible that this is intended behavior, but it is more likely

an omission. This is a strong indication that this layer should be

formulated as a subclassed Layer rather than a Lambda layer.

273/273 [==============================] - 0s 969us/step

273/273 [==============================] - 0s 989us/step

*** Causal Estimate ***

## Identified estimand

Estimand type: nonparametric-ate

### Estimand : 1

Estimand name: iv

Estimand expression:

⎡ -1⎤

⎢ d ⎛ d ⎞ ⎥

E⎢─────────(y)⋅⎜─────────([v₀])⎟ ⎥

⎣d[Z₀ Z₁] ⎝d[Z₀ Z₁] ⎠ ⎦

Estimand assumption 1, As-if-random: If U→→y then ¬(U →→{Z0,Z1})

Estimand assumption 2, Exclusion: If we remove {Z0,Z1}→{v0}, then ¬({Z0,Z1}→y)

## Realized estimand

b: y~v0+W2+W0+W1+W3 | X0,X1

Target units: Data subset defined by a function

## Estimate

Mean value: -0.0007807295769453049

Effect estimates: [-2.2694016 -0.38319397 0.3908844 ... 0.20399475 -0.5440445

4.4043274 ]

Metalearners

[17]:

data_experiment = dowhy.datasets.linear_dataset(BETA, num_common_causes=5, num_samples=10000,

num_instruments=2, num_effect_modifiers=5,

treatment_is_binary=True, outcome_is_binary=False)

# convert boolean values to {0,1} numeric

data_experiment['df'].v0 = data_experiment['df'].v0.astype(int)

print(data_experiment['df'])

model_experiment = CausalModel(data=data_experiment["df"],

treatment=data_experiment["treatment_name"], outcome=data_experiment["outcome_name"],

graph=data_experiment["gml_graph"])

identified_estimand_experiment = model_experiment.identify_effect(proceed_when_unidentifiable=True)

X0 X1 X2 X3 X4 Z0 Z1 \

0 1.634942 -0.075424 -0.767687 1.038749 0.168419 0.0 0.084399

1 0.500951 -0.233160 -0.868487 -1.038950 0.232969 0.0 0.867958

2 -0.558891 -1.476056 -1.001076 0.793516 2.795459 1.0 0.157762

3 0.656949 0.661157 -0.151759 -1.456285 1.416628 0.0 0.447684

4 0.077690 -0.228276 0.463705 -0.528414 0.746399 0.0 0.509194

... ... ... ... ... ... ... ...

9995 -0.935933 -1.225685 0.395988 -0.557393 0.736844 0.0 0.390868

9996 1.278353 -0.602072 -0.587986 0.003152 0.796861 0.0 0.747461

9997 1.171207 -0.414112 0.298943 -0.268608 0.967901 0.0 0.532296

9998 -0.193566 0.261011 -0.987007 -1.410275 -1.183466 1.0 0.768816

9999 1.416659 -0.937048 -2.212555 -0.705596 -0.096399 0.0 0.748053

W0 W1 W2 W3 W4 v0 y

0 0.715595 -1.213655 -1.733133 -1.812450 1.246565 0 -14.874708

1 0.509363 -1.016225 -1.716087 0.532719 -1.290719 0 -11.980213

2 0.268785 0.943569 -2.056643 0.207410 -1.417421 1 -2.605325

3 -0.718373 0.347835 -2.105063 1.089963 0.837798 1 5.346395

4 0.459425 -0.128924 -0.393286 -0.071661 -2.146005 0 -6.887630

... ... ... ... ... ... .. ...

9995 -0.779073 -0.993611 -1.416692 0.419187 0.460952 1 -0.166174

9996 0.314902 -0.431240 -2.471426 0.050317 0.349481 1 -4.108600

9997 -0.957740 -0.356694 -0.757905 1.837526 -0.393220 1 10.545129

9998 0.206553 0.188520 -0.009823 -0.424598 0.726397 1 5.699562

9999 1.425812 -1.725551 -0.883284 0.109924 -0.156964 1 -6.656049

[10000 rows x 14 columns]

[18]:

from sklearn.ensemble import RandomForestRegressor

metalearner_estimate = model_experiment.estimate_effect(identified_estimand_experiment,

method_name="backdoor.econml.metalearners.TLearner",

confidence_intervals=False,

method_params={"init_params":{

'models': RandomForestRegressor()

},

"fit_params":{}

})

print(metalearner_estimate)

print("True causal estimate is", data_experiment["ate"])

*** Causal Estimate ***

## Identified estimand

Estimand type: nonparametric-ate

### Estimand : 1

Estimand name: backdoor

Estimand expression:

d

─────(E[y|W4,W2,W0,W1,W3])

d[v₀]

Estimand assumption 1, Unconfoundedness: If U→{v0} and U→y then P(y|v0,W4,W2,W0,W1,W3,U) = P(y|v0,W4,W2,W0,W1,W3)

## Realized estimand

b: y~v0+X2+X1+X3+X0+X4+W4+W2+W0+W1+W3

Target units: ate

## Estimate

Mean value: 11.005539296781501

Effect estimates: [15.25486783 9.37781661 8.40796173 ... 11.45712636 8.64945964

3.15238619]

True causal estimate is 8.346538950814535

Avoiding retraining the estimator

Once an estimator is fitted, it can be reused to estimate effect on different data points. In this case, you can pass fit_estimator=False to estimate_effect. This works for any EconML estimator. We show an example for the T-learner below.

[19]:

# For metalearners, need to provide all the features (except treatmeant and outcome)

metalearner_estimate = model_experiment.estimate_effect(identified_estimand_experiment,

method_name="backdoor.econml.metalearners.TLearner",

confidence_intervals=False,

fit_estimator=False,

target_units=data_experiment["df"].drop(["v0","y", "Z0", "Z1"], axis=1)[9995:],

method_params={})

print(metalearner_estimate)

print("True causal estimate is", data_experiment["ate"])

*** Causal Estimate ***

## Identified estimand

Estimand type: nonparametric-ate

### Estimand : 1

Estimand name: backdoor

Estimand expression:

d

─────(E[y|W4,W2,W0,W1,W3])

d[v₀]

Estimand assumption 1, Unconfoundedness: If U→{v0} and U→y then P(y|v0,W4,W2,W0,W1,W3,U) = P(y|v0,W4,W2,W0,W1,W3)

## Realized estimand

b: y~v0+X2+X1+X3+X0+X4+W4+W2+W0+W1+W3

Target units: Data subset provided as a data frame

## Estimate

Mean value: 10.430137509460222

Effect estimates: [ 6.19139205 10.84537036 12.99437041 11.06667294 11.05288179]

True causal estimate is 8.346538950814535

Refuting the estimate

Adding a random common cause variable

[20]:

res_random=model.refute_estimate(identified_estimand, dml_estimate, method_name="random_common_cause")

print(res_random)

Refute: Add a random common cause

Estimated effect:12.134496653091002

New effect:12.112653656057013

p value:0.5800000000000001

Adding an unobserved common cause variable

[21]:

res_unobserved=model.refute_estimate(identified_estimand, dml_estimate, method_name="add_unobserved_common_cause",

confounders_effect_on_treatment="linear", confounders_effect_on_outcome="linear",

effect_strength_on_treatment=0.01, effect_strength_on_outcome=0.02)

print(res_unobserved)

Refute: Add an Unobserved Common Cause

Estimated effect:12.134496653091002

New effect:12.088918359215018

Replacing treatment with a random (placebo) variable

[22]:

res_placebo=model.refute_estimate(identified_estimand, dml_estimate,

method_name="placebo_treatment_refuter", placebo_type="permute",

num_simulations=10 # at least 100 is good, setting to 10 for speed

)

print(res_placebo)

Refute: Use a Placebo Treatment

Estimated effect:12.134496653091002

New effect:0.04764782970871019

p value:0.34990266496759126

Removing a random subset of the data

[23]:

res_subset=model.refute_estimate(identified_estimand, dml_estimate,

method_name="data_subset_refuter", subset_fraction=0.8,

num_simulations=10)

print(res_subset)

Refute: Use a subset of data

Estimated effect:12.134496653091002

New effect:12.116950599345797

p value:0.36179771412816353

More refutation methods to come, especially specific to the CATE estimators.